It's been widely publicized that the Federal Trade Commission (FTC) has been sniffing around this whopping $750mil deal since it was announced in November, and at the end of last month two consumer advocacy groups, Center For Digital Democracy and Consumer Watchdog, wrote a joint letter to that regulator making the broad claim that if the deal was to go through “consumers will face higher prices, less innovation and fewer choices.” But, frankly you hear that stuff from watchdog groups on every deal of scale these days, and it kinda seems like part of the hazing process companies go through to get these things done. But I think the detailed, cogent arguments made by Buckingham, and folks like Scott Cleland of Precursor LLC (who made a similar case in a white paper back in mid-December), about the impact on a very specific segment of the mobile ad business (which I frankly hadn't considered), are ultimately more powerful. That said, I'm still reserving judgment on the matter, as I can envision scenarios in these still early days that could mitigate anti-competitive concerns, including; 1) the inevitable evolution of all the app stores and their inventory ecosystems, which may inure more greatly to the benefit of more nimble players; 2) the emergence of innovators with products yielding greater efficacy that will woo publishers and win inventory share; and 3) after what happened in the WAP advertising world I never underestimate the willingness of well-heeled companies to buy into the space with hefty minimum guarantees. But I do say bring on the regulatory scrutiny, especially if its primary objective is to facilitate fair competition. Frankly, I'd be very surprised if the FTC completely blocks this deal entirely, but I definitely think they should take a very detailed look at it and force appropriate divestitures in specific market sectors, if that's what the situation warrants. Let me know what you all think.

Friday, January 29, 2010

Appitalist Wants Regulator To Stop The Google AdMob Deal

Simon Buckingham, best known as the CEO of Mobile Streams, wrote a provocative article on his new Appitalism blog (where he's "Chief Appitalist") on Friday, entitled "Why The FTC Should Block Google’s Merger With AdMob." In the piece he argues that in the new app economy, dominated by the iTunes App Store, in-app advertising has become a critical tool for publishers trying to break through the clutter of 140k+ apps. Currently AdMob and Google dominate this space as the #1 & #2players, followed by Quattro, in a distant 3rd. Buckingham estimates that if Google is allowed to buy AdMob the combined entity would control over 75% of in-app ad market... and that's before Google's new AdSense for Mobile Apps program gets out of Beta. Limited competition in the market will likely lead to increased costs, will potentially stifle the creation of more innovative ad programs and, ultimately, hurt the overall financial health of this nascent, yet vibrant, component of the mobile economy.

Thursday, January 28, 2010

Is The US Worth $540mil To Mobile Game Publishers?

SNL Kagan teased a study that they released today entitled “Economics of Mobile Games," in which they claim the US mobile games market accounted for $540mil in publisher revenue in 2009. The full report (which I'm sure I can't afford) apparently ranks the Top 21 game publishers by US revenue. It would be awesome to have this, but most of us will have to make do with the Top 4 included in their release. Above I've lined up the data they've shared with my last 4 quarters through Q3 2009 for that same Top 4... which includes my (perhaps inflated) $90mil estimate for Namco's mobile business. I've also compared SNLK's total US market size estimate to my latest WW publisher revenue estimate of $1.136bil (which assumes my Top 10 revenue estimate of $795mil equals 70% of total publisher revenue). Let me know what you guys think.

SNL Kagan teased a study that they released today entitled “Economics of Mobile Games," in which they claim the US mobile games market accounted for $540mil in publisher revenue in 2009. The full report (which I'm sure I can't afford) apparently ranks the Top 21 game publishers by US revenue. It would be awesome to have this, but most of us will have to make do with the Top 4 included in their release. Above I've lined up the data they've shared with my last 4 quarters through Q3 2009 for that same Top 4... which includes my (perhaps inflated) $90mil estimate for Namco's mobile business. I've also compared SNLK's total US market size estimate to my latest WW publisher revenue estimate of $1.136bil (which assumes my Top 10 revenue estimate of $795mil equals 70% of total publisher revenue). Let me know what you guys think.btw - did you notice that they make no mention of Snackable's claimed $85mil in revenue?

Nokia Last 9 Qtrs & Q4 Device Volumes By Region

The top chart is in millions. Q4 clearly represents an impressive recovery from recent lackluster reporting periods. The bottom chart is based on a total device volume of 126.9mil units or a 12.2% increase over Q4 2008. Check out more details in Nokia's earnings release.

The top chart is in millions. Q4 clearly represents an impressive recovery from recent lackluster reporting periods. The bottom chart is based on a total device volume of 126.9mil units or a 12.2% increase over Q4 2008. Check out more details in Nokia's earnings release.

Wednesday, January 27, 2010

Tuesday, January 26, 2010

Motricity Pre-IPO Revenue & Net Graph

$mils

I encourage you to peruse Motricity's Form S-1 for fun facts like... 74% of their total revenue comes from AT&T & Verizon Wireless and that "certain of (their) customer agreements expire in mid to late 2010, including agreements with AT&T and Verizon Wireless." Fun, fun, fun.

Monday, January 25, 2010

If The App Store Rocks So Hard Why Are So Many Game Publishers Hurting?

As we all know and as was reinforced in spades by Monday's boffo earnings report... Apple has rapidly and radically revolutionized the mobile content industry with the iTunes App Store. In just 20 months the "fruit company from Cupertino" has created the mobile retail ecosystem that Nokia and the rest of us have been dreaming about since Y2k. There have been beneficiaries of the post-carrier app store revolution (besides Apple) in mobile gaming, which continues to be the biggest category. Notables include some great, small developers like Firemint, which has now sold 2mil copies of its Flight Control game and Lima Sky which is nearing that number with Doodle Jump. But, even some of the big players are claiming great success... Namco has just claimed 23mil App Store downloads, 3 weeks ago Gameloft claimed it had sold 10mil iPhone games and it's no secret that EA Mobile is the biggest App retailer of all. In many respects this should be the glory days of the mobile games space... so why is it then that many established publishers are suffering financially, and that some former luminaries might not survive 2010?

Here are some key factors in my opinion:

Content Clutter: Sure, the App Store is a great platform, but it's a cluttered mess, with over 140k Apps currently competing for the attention of iPhone and iPod touch customers. With very limited promotional real estate it's extremely difficult to create a breakout hit unless Apple has your back or a publisher has the marketing resources to fund substantial off channel promotion.

Price Erosion: As a corollary to the point above, the way many publishers are electing to compete is on price. While you'll see the occasional game as high as $9.99 inevitably the price begins to slip. Unless a game is exceptional, it's difficult to move product above $4.99 and as we all know many of the best sellers are 99¢. If you troll through the ratings comments you'll see that consumers increasingly believe that the price of a game on the platform should be 99¢. For quality publishers who traditionally spend 6-figures on game development (and licenses) that price point makes it exceptionally difficult to realize ROI.

The Carrier Channel's Diminished Importance: Although the majority of mobile game publisher revenues are still coming from carrier decks on Java/BREW feature phones, everybody knows that the consumers with the highest propensity to buy premium content, including games, are abandoning those platforms as quickly as they can get out of their contracts. This sea change is resulting in many publishers seeing 20% year-on-year declines in their Java/BREW revenues. Rapidly, the ability to push product through that klugy channel, by way of having strong relationships with key carrier personnel and having the ability to port games to hundreds of handsets, is shifting from being a competitive advantage, with strong barriers to entry, to being a relatively expensive liability.

Goodbye Recurring Subscriptions: It's a dirty, but poorly kept secret that lots of Java/BREW publishers adored the US carrier channels because of their embrace of the recurring subscription model. You know, buy the game for $9.99 or subscribe for $4.99 per month... which consumers think is such a deal 'til they realize (or don't), when they replace their handset in 15mos, that they spent $74.85 on a game they played 4 times. Publishers are seeing a whole lot less of this scenario, and it's associated lucre, as even the most gullible gamers move to smartphone platforms... where this model doesn't exist. Sure Apple has introduced in-game purchases, which facilitates the up-sell potential of virtual goods, etc. within Apps... but that relies on active decisions by purchasers and will only benefit those publishers that invest in making that a compelling proposition. The "sleeper" subscription model that benefited many game publishers for years is disappearing and those publishers that haven't factored that into their plans and found a way to compensate are going to have a rude awakening.

As a consequence of these factors, my feeling is that the greatest beneficiaries of the smartphone, app store revolution will be small, super-nimble, high-quality developers who elect to move up the value chain and publish to these more democratic platforms. I also believe that the very biggest publishers can survive the transition, and even flourish, by virtue of deep pockets, big brands, big marketing and close, trusted OEM relationships. The many publishers in-between are destined to be victims of this paradigm shift, I'm afraid, unless they learn to behave like their smaller competitors or consolidate into a bigger one.

Friday, January 22, 2010

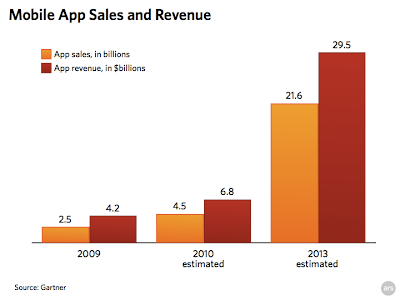

Apple's Path To 3bil iPhone App Sales & Beyond

The 2nd graph, based on Gartner estimates, is for all mobile app stores and Ars Technica believes that in 2010 Apple could be responsible for 3bil (67%) of those sales or $4.5bil in total revenue (of which Apple keeps $1.35bil).

The 2nd graph, based on Gartner estimates, is for all mobile app stores and Ars Technica believes that in 2010 Apple could be responsible for 3bil (67%) of those sales or $4.5bil in total revenue (of which Apple keeps $1.35bil).

Thursday, January 21, 2010

Mobile Streams Announces $11mil in 2009 Revenue

UK-based mobile content retailer (Ringtones.com, MobileGaming.com, etc.), enabler and marketing services company Mobile Streams Plc (MOS) issued a trading statement yesterday, in which they announced that FY 2009 revenues would be in the $11mil range, representing a 20% year-over-year decrease compared with FY 2008. The company is claiming a positive Trading EBITDA... but their 2009 Net (which hasn't yet been disclosed) is likely to be negative. They also revealed that they currently have $2.75mil cash in the bank... down from $3.4mil at the end of June. Hardly a boffo result, so it shouldn't be any great surprise that the stock took a 5% hit in London trading today.

On a positive note, the company did begin to see an increase in revenue from its off-deck mobile internet businesses during 2009. According to CEO Simon Buckingham, "In 2010, these trends are expected to continue as we proportionately increase our revenues from retailing content and apps on the emerging mobile internet. This growth, together with continued cost control, will ensure that we protect our cash reserves in 2010, enabling us to take advantage of commercial and development opportunities as they arise."

But the future of Mobile Streams and its ilk is in some jeopardy. This is one of a handful of companies that sprouted up in the very early days of mobile content (back in 1999) to provide the immensely valuable service of gathering a diverse array of products (music, video, graphics, tones, games, etc.) and then, significantly, getting them all to work on thousands of handsets, hundreds of operator portals and tens of operating systems all over the world. While this is still valuable, especially in markets where feature phones still dominate, their recent revenue softness reflects how significant the shift of mobile content activity to smartphone app stores has been over the last couple of years. Assuming content owners and developers, in established mobile markets, continue to prioritize and publish directly to the top smartphone platforms (iPhone, Android, BlackBerry and Ovi), the roles of aggregators and enablers will obviously be diminished. For Mobile Streams to survive, and perhaps realize renewed growth, I think they'll need to focus on opportunities in developing markets and perhaps the expansion of their mobile internet retailing activities around differentiated content, like adult, which the mainstream app stores don't sell.

Wednesday, January 20, 2010

The Mobile Hotness | Latin America | Courtesy of Matt Garlick

The 2nd installment in Cabana Mobile's series The Mobile Hotness covers some of the latest buzz and trends in Latin America, and is provided courtesy of Matt Garlick, Director of Latin America for global mobile marketing and content technology company 2ergo. Matt is based in Buenos Aires.

- MEF Launches: The Mobile Entertainment Forum launches in Latin America with lead sponsors Playphone, Dada and 2ergo. Its first initiatives will be in Brazil, where the trade association will attempt to address challenges faced by content providers in terms of regulation, taxes, shortcode provisioning, etc.

- Plaza Widgets: América Móvil (194mil subs) launches Qualcomm's Plaza widgets platform to streamline the creation of highly customized, lightweight, connected mobile applications, and (one hopes) simplify monetization…an interesting play aimed at providing subscribers with rich (quasi mobile internet) experiences in predominantly feature phone markets.

- Android Devices: Motorola launched the Milestone with Personal in Argentina, Samsung and HTC launched Android handsets with TIM in Brazil, and HTC launched with Entel PCS in Chile…what will the iPhone vs. Android landscape look like a year from now in Latin America?

- Mobile Advertising: At the end of 2009 Amobee began rolling out mobile advertising services across Telefónica’s Latin American operators while América Móvil partnered with MyScreen to deliver full-screen ads

- Market Saturation: With 100% mobile penetration for Chile and Argentina in place, and Brazil predicted for 2010…carriers will be keen to better understand who their (pre-paid) users are and which pricing models and services help them retain or attract them as they begin to compete for the same customers.

- Mad QR COWdes: Leading Brazilian interactive marketing agency pontomobi is hoping to enhance consumer awareness about 2-D QR codes by tagging cows in this year's Sao Paulo CowParade (see video below)... which is one of the biggest street art events in the world.

Tuesday, January 19, 2010

Is Snackable Earning More Than Glu From Mobile Games?

If the claims of NYC based Snackable Media CEO Eyeal Yechezkell, as reported on TechCrunch and MocoNews, are to be believed then that text-based gaming company made $85mil in revenue last year. That's slightly higher than Glu Mobile's last 4 quarters (Q4 08 - Q3 09) and would make Snackable the #4 mobile games company in the world by revenue on my chart... perhaps even #3 if my Namco Mobile estimate is inflated. Apparently there's still a healthy business in $9.95 monthly recurring subscriptions for text-base quizzes and versions of "Deal Or No Deal". I wished I was more shocked that consumers continue to sign up for these kinds of subscriptions... but I've come to realize in my old age that there's more than one sucker born every day. However, the overall numbers discussed here do shock me and, as usual, I'm more than a little skeptical. What do you guys think?

Nokia Preempting Apple Hypefest With Jan 21st Ovi Press Event in London

I hope there's more to this than a platform announcement about Ovi 2.0 and a pre-recorded greeting from Dave Stewart or Spike Lee.

I hope there's more to this than a platform announcement about Ovi 2.0 and a pre-recorded greeting from Dave Stewart or Spike Lee.

Monday, January 18, 2010

How IDC Slices A $287mil US Mobile Ad Pie

The chart above features the market shares of the top US mobile advertising companies (based on their % of revenue in a $287mil market) as included in the report “Mobile Ad Market Share Estimates Show Yahoo and Microsoft Must Follow” released by industry analyst IDC in the wake of the $750mil Google-AdMob deal. This report was met by some controversy, as Mobile Marketer revealed in a story at the end of November. Companies like Jumptap immediately claimed that their revenue was "drastically understated." But, of course, neither Jumptap nor any of the other companies covered stepped up to reveal what they were actually making... because that's not how private companies in the mobile space roll (fantasy is usually sexier than reality). Frankly, I usually assume all whisper and analyst numbers in this space are inflated and I think this report is no exception.... I don't think AdMob made $40mil in 2009. Nonetheless, the report, suggests correctly I believe, that with the AdMob deal done (and now with AOL/Quattro) both Microsoft and Yahoo (who apparently once courted Millennial) are in the hunt for acquisitions in early 2010 so they can challenge Google's potential 24% market share. I'm looking forward to lots of crazy valuations... which could be a good thing in the short-term if the acquiree's VCs realize handsome paydays and, consequently, are motivated to inject more risk capital into the mobile content market.

The chart above features the market shares of the top US mobile advertising companies (based on their % of revenue in a $287mil market) as included in the report “Mobile Ad Market Share Estimates Show Yahoo and Microsoft Must Follow” released by industry analyst IDC in the wake of the $750mil Google-AdMob deal. This report was met by some controversy, as Mobile Marketer revealed in a story at the end of November. Companies like Jumptap immediately claimed that their revenue was "drastically understated." But, of course, neither Jumptap nor any of the other companies covered stepped up to reveal what they were actually making... because that's not how private companies in the mobile space roll (fantasy is usually sexier than reality). Frankly, I usually assume all whisper and analyst numbers in this space are inflated and I think this report is no exception.... I don't think AdMob made $40mil in 2009. Nonetheless, the report, suggests correctly I believe, that with the AdMob deal done (and now with AOL/Quattro) both Microsoft and Yahoo (who apparently once courted Millennial) are in the hunt for acquisitions in early 2010 so they can challenge Google's potential 24% market share. I'm looking forward to lots of crazy valuations... which could be a good thing in the short-term if the acquiree's VCs realize handsome paydays and, consequently, are motivated to inject more risk capital into the mobile content market.

Velti Forecasts $106mil in 2009 Revenue

UK mobile advertising outfit Velti Plc (VEL), the company that bought AdInfuse last year, got a jump on FY 2009 earnings season by forecasting revenues of over $106mil... which represents 24% year on year growth. The company claims to have run over 2k campaigns for over 450 brands during the last year and indicated that demand for its products remains strong. While the company is trying to spin the earnings as "in-line", many analysts had them pegged in the $115mil range, so the company's stock took a 3% hit in London trading today. It'll be interesting to see the rest of the numbers when they report full details in the next few weeks. Despite the near miss, Velti is probably the biggest of the mobile advertisers, with revenues more than double those of hyped US plays like Millennial and AdMob (in the process of being acquired by Google for $750mil) and at least 5x the revenues of Quattro (which is being acquired by Apple for $275mil). Oh, and by the way, these guys actually turned a (real) net profit last year. One wonders why, in light of Velti's performance and the recent frothy valuations of other mobile advertisers, that its market cap is only around $153mil.

Friday, January 15, 2010

Schlage LiNK Makes Your House Less Stupider

(Cabana Mobile is all about mobile entertainment, but unfortunately I haven't been entertained by much mobile entertainment in the last few days... so you'll have to excuse me for going off on a bit of a tangent...)

But perhaps that's all beginning to change with the help of mobile technology (angels sing). One of the most minty things I experienced at CES (which I mentioned my recap) was a demo of the Schlage LiNK remote management system, that allows homeowners to open, close and monitor locks, adjust temperature, turn lights on and off and access security cameras in their homes from a remote BlackBerry, iPhone or Windows Mobile handset. Imagine, if you will, the hilarity that'd ensue when your wife's boyfriend or your girlfriend's girlfriend shows up to raid your fridge while your Christmasizing with the inlaws in Boise... you could freak a freak out with that Bold, lemme tell you. The system makes use of the Z-Wave wireless protocol to control the individual devices. Components are available for sale at places like Radio Shack, or you can get a starter kit with router, door lock light dimmer through Amazon for about $285. Monthly subscription from Schlage costs $12.99 a month. Until Schlage sends me a kit to review at home, check out this demo from Crackberry... and let me know what you think.

Wednesday, January 13, 2010

App Utility Across Smartphone Platforms May Be Equalizing

Craig Dalton over at Mplayit had an interesting post on his blog this morning highlighting some data his company just released from an activity survey of 42k visitors to their Facebook mobile discovery apps (e.g. iPhone Arcade) at the end of 2009. The company compiled the favorite apps of users across 3 smartphone platforms (iPhone, Android & BlackBerry) in 6 key content categories (excluding games)... and the results (see above) were remarkably similar. Craig's thesis is that, in terms of utility (in these categories), the platforms are beginning to approach parity for users. I think he might be on to something. Furthermore, reading this raised a question in my mind about a challenge the iPhone ecosystem may be beginning to face: At what point does the shear volume of Apps, many of them free and/or crap, on iTunes begin to make the platform less attractive to time constrained users who want to maximize the utility derived from their device? In other words... at what point is too much selection a bad thing? Let me know what you think.

Monday, January 11, 2010

Dredging The CESpool For Cool

So, I'm back from Las Vegas with a lighter wallet, no voice, potential liver damage and some decent business prospects. Good show, good times. I've aways contended that it's hard to get perspective on the entire beast that is CES when you're on the ground, living it... but for what it's worth here are the things that I thought were cool, interesting or notable from the slice of the show I experienced:

- First, props to the nurse at the First Aid Station at the Las Vegas Convention Center, who by virtue of providing me with an isopropyl soaked towelette was ultimately much more helpful rectifying my latest BlackBerry Bold trackball crisis than the charming yet useless folk in the RIM booth.

- 3D TV is way cooler than I expected, especially the full HD version (1080p in both eyes). But, it is still hard to fathom kickin' it in active 3D glasses along with 22 of my closest friends during a Superbowl XLV, or a Superbowl L party for that matter. I think Samsung is on to something with the glasses-less solution. The good news in the short term is that excitement around this niche should make that sweet non-3D 55" LED set I'm coveting much cheaper.

- Thanks Nokia booth guy for the great demo of the N900. Slick device. I particularly liked the social networking topscreen widgets (like MotoBlur) and thought the Flash 9 enabled browser was awesome. Now go and get yourselves a carrier subsidy you sillies.

- Slates, tablets, eReaders galore... some like the Kindle except better, like Plastic Logic's Que proReader, and some that are more rich media friendly the the HP slate. There's a lot of froth and fear in this product sector that I'm convinced (and reliable sources I spoke with agreed) is about to be defined (on Jan 27th) by Apple.

- I'm happy to report that based on the balance of parties there's evidence to suggest the AVN is virile of spirit (if not of revenue) in the face of potentially withering challenges that industry faces from an onslaught of free digital services and its cultural destigmatization. Didn't get to spend any quality time at that show, but I did get to attend one of the aforementioned parties courtesy of some cool folk at Gawker, and I was gonna say it didn't suck at all, but...oh never mind....

- Android, Android, Android... the exuberance continued into the show following Google's Nexus One event last week. The fact that Flash 10 was announced to be coming to Android browsers didn't hurt. (Hopefully this will push Apple over the hump with Adobe). On the Android handset front I heard some strong positive buzz from industry insiders about the Sony Xperia X10 device (see demo below), that will unfortunately sell like 2 units in the US if the SE can't get any carrier love.

- I like to say I'm into architecture, so I thought my mind would be blasted by the newly opened City Centre property... but no so much. I felt that it took some modern concepts from a dream team of kick-ass designers and plugged them into a tired LV model (set back hotels, promenade mall, etc.). Instead of feeling original and exuberant, it felt formulaic and strangely anachronistic given its embrace of super-premium Eurotrash retailers and it's cookie-cutter (though dark) casino. On top of that, several locals I spoke to expressed hatred for the already notoriously crap attitude of the staff. I did have an Eric Schmidt sighting there on Friday, which felt as much like a check-the-box as the property itself.

- Samsung blew it on the mobile front by not showing their highly anticipated Bada S8200 featuring their Bada OS (yeah! another smartphone OS?). I think they had the most impressive booth at the show, but overall I must say their handset selection made me long for another Red Bull (without Vodka this time).

- Unexpected superawesomeness in the form of the Schlage LiNK demo in the RIM booth. They have system where you can use your BlackBerry (or, presumably, any other web enabled phone) to remotely access and activate your door locks, temperature controls, lights and remote cameras in your house. While my initial thoughts tended toward hijinks, in retrospect this system may be one of the more useful innovations demonstrated at the show.

- Lenovo had some bad-ass looking netbooks, including the tabletesque, capacitive screen S10-3t. But you know, in terms of netbooks that Nokia Booklet 3G that was deployed all over the Nokia booth maybe the netbook eyecandy du jour.

- There was a lot of excitement about the Boxee Box (made by D-Link) that allows consumers to access the internet content on their TVs without a computer. Uh, er... wasn't that called WebTV? I'm not convinced I should be excited.

- Sprint's Overdrive 3G/4G portable hotspot device has a lot of potential...like Verizon's MiFi but faster. However, it's not even worth considering in LA til almost 2011, when their WiMax network rolls out here.

I'll add more if I think of them... in the meantime I'd love to hear what impressed you. Let me know.

Wednesday, January 6, 2010

Cabana Mobile Is At CES Thursday & Friday

...I'll tweet from Las Vegas and summarize my observations on my return. I hope to see some of you at the show.

Is This How Gameloft's 10mil iPhone Game Sales Break Down?

CLICK ON IMAGE TO ENLARGE

Jon Jordan at PocketGamer.biz had a story today covering Gameloft's announcement that they've sold 10mil iPhone (and iPod touch) Apps since the App Store opened 18mos ago, in which he points out that the French publisher "didn't reveal any per title sales figures." Well, considering my recent fascination with correlating User Ratings with downloads, I thought I'd take a stab at decoding this... just for kicks. In my post on Dec 16th I told y'all that based on some conversations with publishers I was getting comfortable with the notion that each User Rating on a Paid App accounted for 75 downloads as a rule of thumb... I then went on to perform some calculations on iTunes Rewind 2009 to support my thesis. This seemed to work pretty well, as long as I adjusted the numbers to show that casual games downloaders have a lower propensity on average to post a User Rating and that those who downloaded games for gamers have a greater propensity to post one... which made intuitive sense to me.

Well, in looking at the total reviews of Gameloft's 56 Paid App titles as they relate to their 10mil download claim, assuming their title mix is typical of all Paid App games in the store, then it looks like my average number of 75 may have been a little high. Gameloft games have received a total of 163,931 User Ratings and if I divide 10mil by that number I get 61... so maybe that's the right correlation. I still think adjustment for casual and gamerly games are required, but for the spreadsheet above I simply decided to apply the number equally across all titles. The spreadsheet is sorted by downloads and the estimated revenue is based on today's price (so take that with a grain of salt), as opposed to the Estimated Average Price over the game's lifetime I'd use if I had more time (remind me to hire a staff when I get rich off this blog... right). One thing that this does seem to show (if this is correct) is that Gameloft actually does have 1 title with over 1mil paid downloads... "Hero of Sparta" which launched in December 2008.

Tuesday, January 5, 2010

Is Glu's de Masi Move Part Of A Hands-On Hook-Up?

I've been racking my brain for the last couple of days trying to make sense of the news that Niccolo de Masi is leaving Hands-On Mobile, after just 3mos as its CEO, to run Glu Mobile. My first thought was that Hands-On was in such disarray, and so late to the smartphone game, that the restructuring I hoped was afoot turned out not to be worth pursuing in the end. My second thought was that Glu got so desperate in their protracted CEO search that they put more money on the table than a 29 year-old could possibly refuse... 'til I read their latest 8-K. Then I had a conversation today with an industry veteran who posed a novel, and ultimately, more interesting theory. What if de Masi is bringing Hands-On with him? What if this move is the precursor to a merger between the two companies?... now that's juicy!

From Glu's perspective this could be attractive because Hands-On allegedly still has a pile of cash left in the bank from the $29mil sale of its Korean division to EA in May 2008. For public Glu, with a depressed stock price vacillating on either side of $1 and a healthy appetite for cash, this could be an attractive fix. Glu would also benefit from Hands-On's valuable World Poker Tour license, which has been a cash cow since 2005, and its legacy Guitar Hero licenses (also big earners), which would be a nice complement Glu's newly launched Guitar Hero 5 title. For the investors in Hands-On, including Executive Chairman Dan Kranzler, this could finally be a way to go public... like they've been planning since the mobile paleolithic. It would also give Hands-On much improved smartphone capability (an area where Glu is finally getting its shit together) and restore its once impressive international distribution capabilities. Moreover, this move could create a real competitor, another $100mil+ (or close to it) game publisher, in an industry segment that's recently looked a lot like a two horse race between EA Mobile and Gameloft.

What do you readers think?

Monday, January 4, 2010

Breaking: Niccolo de Masi Named Glu Mobile CEO

Whoa! Former Monstermob wunderkind, and most recently Hands-On Mobile CEO, Niccolo de Masi has just been named President and CEO of Glu Mobile. This is shocking since he was just named to the head post at Hands-On Mobile this past October. It makes one wonder what on earth is happening at that long-struggling publisher. More to follow... Meanwhile according the Glu Mobile press release:

In connection with the appointment of Mr. de Masi as Glu’s new President and CEO, the Compensation Committee of Glu’s Board of Directors awarded Mr. de Masi a non-qualified stock option to purchase 1,250,000 shares of Glu’s common stock pursuant to Glu’s 2008 Equity Inducement Plan, which is a non-stockholder approved plan. This stock option was granted to Mr. de Masi on January 4, 2010 and has an exercise price equal to the closing price of Glu’s common stock on the NASDAQ Global Market on such date.

iSlate Will Help Apple Dominate ePublishing

Earlier today WSJ's John Paczkowski revealed that Apple is hosting an event in San Francisco on Weds Jan 27th (2 weeks before Macworld 2010), presumably to launch the hotly anticipated tablet device the technorati confidently call the iSlate. There's been rampant speculation for months in the tech press and blogosphere about this product's form factor, OS, UI/UX, hardware components, etc., but I think the most interesting discussion is around the digital content category it'll help Apple dominate. The iPod quickly allowed them to control digital music and the iPhone mobile apps... so what will it be with the iSlate? Stu Dredge had a great post this morning theorizing about which games would be best suited for a tablet-like device, and there's been a lot of talk about how its rumored 10" screen will make it the ultimate portable video player. While I think the iSlate has potential to be awesome for both of those categories... the big win for Apple will be in electronic publishing. I'm confident Apple has it's sites firmly set on Amazon's hot-selling Kindle, and believes it has the chops to deliver a much better consumer experience (the bar isn't set too high, frankly). Imagine all your favorite books, magazines and newspapers available for sale or subscription through iTunes, at super-reasonable prices (an Apple hallmark), that can be enjoyed in full color, with intuitive interactive tools and sharing features. Assuming they can get deals done with all the major publishers (talk about old media, oy vey!), that the hardware isn't prohibitively expensive (~$500) and that they also make ebooks & emags available for legacy devices (e.g. the iPhone), I think within 1 year they could easily dominate the space. Unless I've got this all wrong, publishers, particularly those on the newspaper/magazine side getting massacred by the online ad-supported business model, should be kissing Steve Jobs' (feet) about now. Meanwhile, I suspect Bezos & company are chewing copious fingernails in anticipation of the Jan 27th event.

Subscribe to:

Posts (Atom)